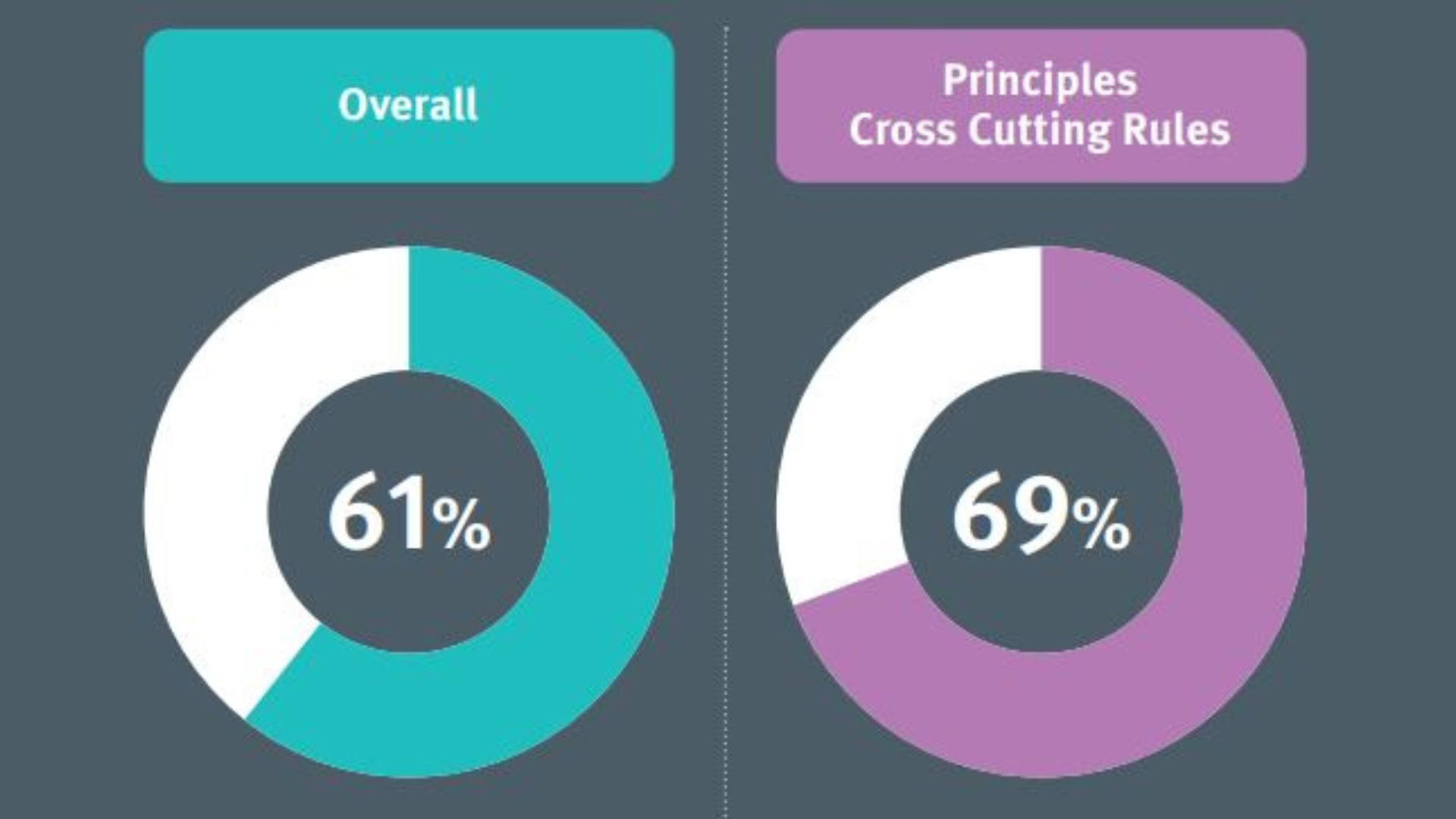

Many firms are making good progress towards the production of their first Consumer Duty board reports for the end of July deadline. The question remains however about whether the reports will succeed in driving the kind of cultural change the Financial Conduct Authority is looking for. Many agree that the notion of treating consumer outcome discussions on a par with financial outcome discussions is a practice that most boards will struggle to adopt. This being the first board report, there is no consensus on what good looks like, as firms feel their way into what will satisfy the FCA’s expectations.

Ultimately, while there is a lot of talk about training front-line staff on how to integrate Consumer Duty into their activities, boards themselves are likely to benefit from training on how to achieve the cultural embedding the regulator is expecting. The appointment of a Consumer Duty champion as a non-executive role on the Board is seen as a good way to ensure that these discussions are occurring. Equally, this could be a double-edged sword if boards see the mere existence of the champions, complimented by a one-off annual discussion of their Consumer Duty report, as sufficient. Boards should conduct rolling assessments of the Consumer Duty outcomes over the year, with the annual report acting as a culmination of this activity rather than a ‘one and done’ approach.

The principles and outcomes-based approach to Consumer Duty means there are different expectations on insurance and financial advice businesses. Indeed, even within the sectors themselves, there is an expectation on firms to implement Consumer Duty, and to shape their board reports to the uniqueness of their business, target market and customer segments.

In our view, financial advisers arguably confront a simpler task, as their proposition is wholly oriented around understanding the outcomes (goals) that a consumer seeks and putting a financial plan in place to try and make it a reality. Those circumstances give rise to many quantitative and qualitative options with which consumer outcomes can be measured and reported against.

This feels trickier for insurance. A product which we all have but hope never to use, so the concept of a good outcome becomes vaguer. Post sale, making a claim is often the only time a consumer interacts with the insurer and the policy they have purchased. Can the provision of insurance and the peace of mind it offers be considered a good outcome? Satisfying themselves on the price and value outcome may therefore take greater emphasis in insurance board reports.

The claims process is therefore where board reports may focus. Are the policy documents intelligible? Is the claims process efficient and achieves a resolution for the consumer in a timely manner that mitigates stress in a situation whereby every consumer could be considered vulnerable. In a claims environment it can be that many external parties influence the claim – claims management companies, lawyers, credit hire, loss adjusters, repairers, third-party insurers, etc. Is the end consumer kept central to the outcome?