Friend or foe? Threat or ally? What will so-called robo-advisers do for the future of the advisory market?

There’s been much talk of robo-advice recently but will robo-advice disrupt the market and what impact will it have on Financial Planners, Paraplanners and providers?

Should Financial Planners and providers launch their own robo-advice service? Can robo-advice work alongside a fully-fledged human advice service? What are the benefits and risks?

This article, first published in Financial Planner on 29th March, 2016, looks at these questions as well as the history and robo- advice’s role in other countries, such as the US where it is already established.

Robo-advice. Never have two small words grabbed so much attention in our industry in such a short space of time. Government, regulator, providers, advisers, fintech disruptors, media commentators, even some consumers have an opinion about the rise of the robots.

Robo-advisers have been making headlines for several years now in the US, not least due to the millions of dollars of venture capital investment being poured into the sector. Today, there are over 200 robo-advice propositions in the US, often founded by young, tech-savvy entrepreneurs out of Silicon Valley. But it has been the arrival of automated investment propositions from major brands such as Vanguard, Charles Schwab, and Fidelity which has validated the robo-model as a legitimate alternative to the traditional face- to-face channel. With trusted brands and deep marketing pockets, these robo-providers are acquiring multi-billion dollars’ worth of assets; for example, Vanguard’s Personal Advisor Services has reportedly grown to $31bn AUM (as at January, 2016) since launch in May 2015.

What really is robo-advice?

On this side of the Atlantic, things are a little more complicated. If you believe what you’ve read in the press over the past year you could be forgiven for thinking robo-advice applies to almost any remotely digital financial services proposition, regardless of whether any advice is actually part of the service.

A definition I like for the UK market, is this:

“A streamlined, automated, and simple to understand process-driven advice service, delivered over the internet, supported by telephone, web chat, or video service, and which aims to address the straightforward needs of consumers at lower cost.”

There are a number of important components in this definition but the key one – certainly for the UK – is the word advice. In this case, restricted, simplified advice, but advice nonetheless. This is very different from the ‘lighter regulated’ US, where the term robo-advice covers a far broader church, and is typically used to describe any automated investment service helping the investor make an investment decision.

The British robots

As a result, things are taking a little longer to develop over here and only a small number of firms meet our UK robo-advice definition: Parmenion Interact (a white label service which powers many adviser robo services, such as Wealth Horizon and Fiver a Day), Money on Toast, and Wealth Wizards (which underpins the LV= retirement income service, CORA) are notable examples.

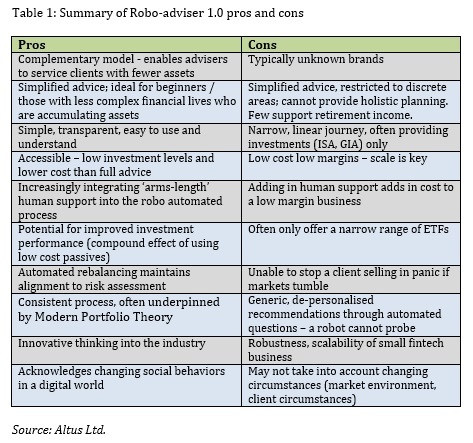

These original Robo-adviser 1.0 propositions have been developed by small, entrepreneurial fintechs – so called digital disruptors – using technology to re-invent traditional processes and disrupt the traditional face-to-face adviser channel, their argument being that digital solutions can guide people’s investments more transparently, objectively and consistently, provide better longer term returns, and crucially at much lower cost than a human adviser.

Initially targeting the Millennial generation or people with less complex financial affairs, many (though certainly not all) of today’s robo 1.0 propositions provide broadly similar services, as illustrated in table 1 below:

Cheap as Chips

Cost, of course is key and eVestor, for example, a new UK robo proposition being launched later this year, will be marketed at 44 bps all in. That’s 35 bps for product, advice, and investment, and an average of 9 bps for fund charges. Over in the US, and amid some controversy concerning the underlying costs of the service, Schwab is marketing their Intelligent Portfolio service at zero cost. And just a few basis points for the ETFs.

It’s the simplicity, transparency and cost of the robo model that has got the Treasury and FCA excited, as they look to address the ‘advice chasm’ in the UK. Through the FCA’s Project Innovate and ‘safe harbour’ Regulatory Sandbox, and the Treasury-led Financial Advice Markets Review (FAMR), the regulator and Government are looking to the fast-developing UK fintech sector to deliver the disruptive innovation needed to lower the cost of, and ease of access to, advice.

But despite the clever thinking in some of the Robo 1.0 propositions, I’ve been left with the feeling on more than one occasion that as a potential customer I have to really want to get to the end of the process.

Too many words, too many questions, too boring.

I’m pretty certain this isn’t what Harriet Baldwin has in mind when she talks about “disruptive innovation”, but it’s not necessarily all the fault of the robos, to be fair. I’m looking to the outcomes of the FAMR recommendations – as well as clever and better use of data sources and gamification techniques – to address this, otherwise the industry will struggle to make the game-changing innovation being demanded.

New Year revolutions

Despite the barriers, 2016 will be the tipping point for automated advice services, and we will witness a multitude of robo-style propositions coming to market. I am personally aware of over fifty in development! Announced in the press and already on the blocks: eVestor, Moo.la, and Nutmeg’s new advised proposition, while Bellpenny and SimplyBiz have both signaled their intent. Not surprisingly some of the US robos are being courted by UK firms wanting to get a new proposition to market, though with different regulatory environments it’s a tough ask.

Other firms developing full robo solutions or aiming to play a part in the wider robo- ecosystem include MoneyFarm (the Italian robo now with FCA approval to operate in the UK), Wealth Objects, and technology providers’ eValue, Intelliflo, Distribution Technology and Finametrica. While several will undoubtedly be labelled ‘me too’ propositions on the robo bandwagon, others will launch propositions which are more considered, offering broader and richer functionality, or more specialised solutions.

2016 will be the year that Robo 2.0 begins to emerge. Goals-based propositions offering a wider range of product solutions will provide reasons for customers to return. The use of creative content, tools and calculators, and the opportunity to view a current, aggregated view of their entire personal finances and debts will all help customers better engage with their money, and make the decisions needed to achieve their financial ambitions. Other propositions, such as Motif Investing’s active trading service, or Money on Toast’s new £250,000+ proposition, will inspire others to develop differ- entiated propositions, focusing on particular niche markets or solutions.

Return of the Banks

Having been encouraged back into the advice sector by FCA and Treasury developments, the opportunity for High Street banks to re-engage with their mass-market customers cast adrift post-RDR is a logical next step, and a number have already stated their intent. Despite nervousness around systemic issues if the robo-algorithms prove to be fallible, this is too big an opportunity for the banks to ignore. But without the in-house expertise, or time, to develop Robo 2.0 solutions what will the banks do?

A likely outcome will be a partnership or acquisition of one of the existing robo solutions, and we’ve already witnessed examples of this in adjacent sectors: Aberdeen’s purchase of Parmenion, LV=’s majority investment in Wealth Wizards, Investec’s acquisition of Jemstep, and Blackrock’s purchase of FutureAdvisor. Other large organisations – blue chip employers, EBCs, retailers, affinity groups and the banks themselves – are all likely to follow a similar path to provide a low cost service to their customers or members. This marriage of big brand with digital disruptor brings together distinctive but complementary skillsets and capabilities:

- Trusted, well-known brands with significant numbers of existing mass market/mass affluent customers, many in serious need of advice

- Small fintech entrepreneurs with expertise, an innovative mindset, a single-minded approach, and the technology.

Whether the big banks can balance these two remains to be seen.

Different strokes for different folks

Originally dismissed as too simplistic and aimed only at Millennials, the UK adviser community has recognised – as it did in the US – that robo solutions are not just for the younger generation, and that they provide both an opportunity and a threat if they don’t respond.

Typically marketed under a different brand name and run in parallel to the full advice business, there is a range of robo options to choose from, depending on the firm’s longer- term objectives, target client segments, and the role they wish to play in the value chain:

- simple white label of existing robo tech and investment proposition – easiest and quickest way to market; no regulatory responsibility; lower rewards

- license / configuration of existing tech solution and integrate with existing capabilities – longer, more expensive route to market; more control; a degree of differentiation; regulatory responsibility; greater rewards

- buy software or partner with a fintech firm – the longest, most expensive route; a differentiated solution; regulatory responsibility; much greater rewards (if you get it right).

A stringent RfP process followed by detailed due diligence of short-listed potential technology and / or investment partners is critical. Importantly, is your suitor geared up to the evolution of the market, rather than just responding to the needs of the market today?

Some adviser firms of course will not wish to develop their own robo proposition, believing a robo service would dilute their brand reputation, or take focus away from their existing higher value business.

Such firms may be better placed to invest further in technology to automate or digitally enable as many processes as possible in their full advice proposition, to achieve greater efficiencies, reduce costs, and speed up the process, all of which benefits the end client.

Be prepared

It can be difficult to agree the best course of action for a firm, but beware indecision. There is enough evidence globally that the way financial services are purchased and serviced is rapidly changing.

Look at the apps you’ve downloaded onto your smartphone – banking, Uber, Spotify, Skype, Netflix, AirBnB, betting – to see how you are already part of the disruption taking place in other sectors.

The next wave of robo disruption – Robo 3.0 – will be from the outside, and I’ll look at this in more detail in a future article – Robo as a Platform.

This article was first published in Financial Planner on 29th March 2016.