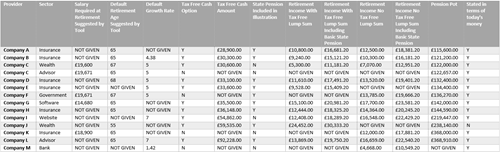

Using the most popular on-line pension illustration tools from some of the top insurance and wealth management companies and even the Money Advice Service Altus calculated what that person was likely to get at the point of retirement. The results highlighted a massive disparity.

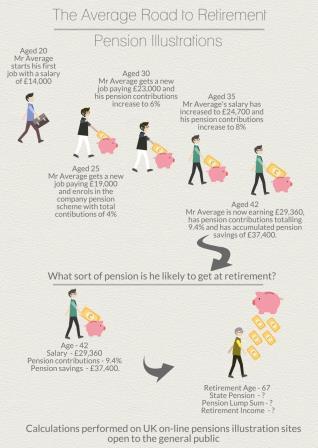

Altus’ consultants took an average person earning £29,360 with existing savings of £37,400 at age 42 with pension contributions of 9.4% from salary. The results highlighted a massive disparity in the potential size of the pot at retirement with the most pessimistic provider quoting just over £115K and the most optimistic quoting a little under £370K.

The table below is based on the following scenario details:

current age – 42, retirement age – 67, current salary – £29,360, existing pot – £37,440, contributions employee – 0, contributions employer – 230.

Methodology

- Contributions were treated as being paid through salary sacrifice so were treated as 100% Employer Contributions.

- Contribution rate was calculated as 9.4% of current salary based on weighted average of combined employee and employer contribution rates published in the ONS Occupational Pensions Survey 2013 published in September 2014.

- Average Salary was based on figures from the ONS Annual Survey of Hours and Earnings.

- Existing pot value was based on calculations of contributions made from age 25 at varying contribution rates, investment growth compounded at 3% and salary growth increasing in line with figures from the ONS Annual Survey of Hours and Earnings.

- Providers chosen from a list of returns from the Google Query Search “Pension Illustration Tool” choosing UK providers only and selecting only providers offering an open service with no registration required.

- Default growth rate represents the rate given as the most likely growth rate by the provider. Where only one rate was shown this was chosen, where a choice of rates was given the mid range or most likely rate was chosen.

- Calculations were all based on a 42 year old male with no dependants or spouse retiring at age 67 with a current salary of £29,360, existing pension savings of £37,440 making contributions through salary sacrifice at a combined employee/employer rate of 9.4% seeking the maximum allowed tax free lump sum and a flat rate income in retirement.